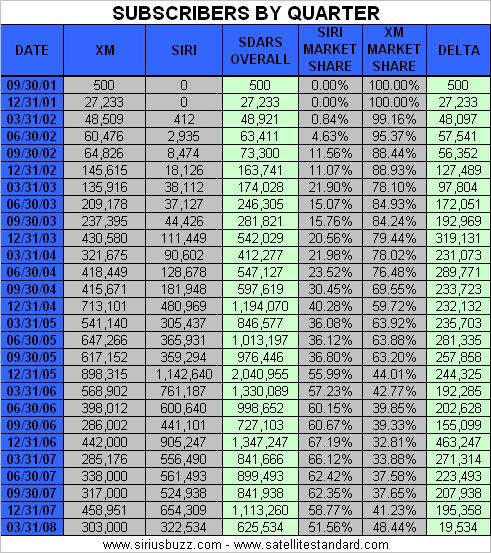

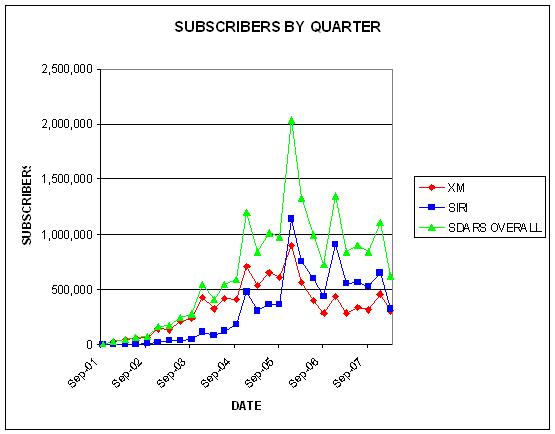

The Subscriber Picture

The numbers are the numbers, and the charts speak for themselves.

Catch Sirius Buzz Radio Live Each Thursday at 10:00 PM Eastern – Or Catch A Replay Of Any Show

Position – Long Sirius, XM.

The numbers are the numbers, and the charts speak for themselves.

Catch Sirius Buzz Radio Live Each Thursday at 10:00 PM Eastern – Or Catch A Replay Of Any Show

Position – Long Sirius, XM.

Please do your best to keep comments interesting, to the point, and topical. Abusive, inappropriate, and blatantly self promotional posts may be edited or removed. If you have a question or an off topic comment, that is what the forums are for!

Just found ... looking for antenna options for '77 F150Tuner Location?

Just found ... looking for antenna options for '77 F150Tuner Location? Baba Booey Turns 25

Baba Booey Turns 25 SiriusXM Announces Additional $2 Billion In Stock Buyback

SiriusXM Announces Additional $2 Billion In Stock Buyback SiriusXM To Launch Bill Carter Show

SiriusXM To Launch Bill Carter Show SiriusXM Settles Royalty Lawsuit For $210 Million

SiriusXM Settles Royalty Lawsuit For $210 Million

It would be interesting to chart the growth in GM subs in absolute numbers and as a percent of the total subs. GM is delighted to install as many subs as XM wants since between the $100 per install and the 30% revenue split they make a ton more on these installs then XM does at the end of the day. The pedal to the medal on these GM subs is the only reason subs total are up at XM.

>>>The pedal to the medal on these GM subs is the only reason subs total are up at XM.

GM announced that they had surpassed 4 million XM installs at the end of 2006 — and that they would install 1.8 million in 2007. They further announced that they would install 2.5 million in 2008.

Doing the math, 4 million + 1.8 million + 1 million(partial for 2008) = 6.8 million installed to date (very rough estimate). Multiply that by 52% conversion = 3.5 million GM subs.

Then take out churn over the last 4 years on these subs… roughly 1.7% each month (scaling up from 100K – 5 years to today) — I’d say that there are roughly 2.5 million GM subs right now on the road, out of XM’s 9.3 million subs.

XM says they have 3.86 million OEM subs currently, so yeah… roughly 65% of XM’s OEM subs are GM subs right now, I’d estimate. Which is about 27% of all of XM’s subs.

—

P.S. – Regarding the pedal to the medal comment… XM has preannounced that GM is installing 2.5 million XM’s this year; Honda is at approximately 850K; plus Hyundai, Infiniti, Nissan, Toyota and Lexus are combining for another 1 million in 2008. Again, this was preannounced at various times. These combine to about 4.3 million installs for the year.

XM announced on their Call yesterday that they had 1 million installs in Q1 — which supports the 4.3 million for the full year estimate (Q3 and Q4 will be ramping up higher).

Of the 1 million XM OEM installs in Q1 this past quarter — I’d estimate that GM was approximately 600K~650K of those, with the other 400k+ coming from the others.

Pedal to the medal? Or more gradual? It was 1.4 million installs in 2005; it was 1.5 million in 2006, 1.8 million in 2007 and now 2.5 million in 2008 (big jump)… regardless, it is expensive as hell.

I do disagree that GM is the only reason that XM is up in subs for the quarter, though… of the 800K OEM Gross in Q1 — GM was a lot of those, but the others are ramping too now… namely Nissan, Infiniti and Hyundai, plus more Honda. Note that a 700K full year increase for GM installs of XM, breaks down to just 175K more each quarter. So it’s more than just GM.

–

noone….

At this point the rev share is maxed out on the GM deal. Many consider the rev share payment to be between $5.00 and $5.50 per month for all installs after the 6,000,000th install.

That would put it between 38% and 42% of the current subscription price.

Lots to respond to –just a few points–as I said elsewhere in the past XM mgt. has said that 3.00 per sub per month was the max rev share (when they increased monthly prices to match SIRI they said that GM only got 30% of the prior number and did not share in the increase). Who knows what is true as they over time abandon prior comments with out explanation. As for the churn issue it was originally in the 1.4 range and later went up as for GM OEM’s in the last 12 months that became subs I would say you have lost only 6% due to churn. As for pedal to the metal the early 2006 game plane was for 2007 to go only slightly up from GM 2006 and for 2008 to be flat. The increase decided on in late 2006 (when neither Oprah nor Toyota brought the expected subs) has been an incredibly bad idea. They would have been much better off hold GM flat and cutting costs. When you figure their cost of funds over the next four years the NPV of these GM subs over their life may be as little as 50 bucks to XM and worth about 400-500 each to GM. All in all another terrible quarter (BTW I am nt so sure the 53% conversion in recent quarters was not affected by some very low ARPU 12 month promotion deals they did on new cars–since these are revenue paying I think they may not count them as promos but real subs and since Nate and Gary will basically tell you nothing in the recent CC’s one can not know).

Keep on cheerleading–you certainly have the credentials to do so.

noone….

>>>>>XM mgt. has said that 3.00 per sub per month was the max rev share (when they increased monthly prices to match SIRI they said that GM only got 30% of the prior number and did not share in the increase)

The GM deal had and has always had a sliding scale on revenue share. In the past what XM management had stated was that the rev share was based on the $10 per month price, and that the price increase was money that GM did not participate in. You can review the GM distribution agreement and see that after the 6,000,000th installation that the rev share maxed out at 55% of the $10 per month price.

William Kidd was one of the first analysts to see that GM subs took a long time to become profitable. This is still the case today.

XM calls the average life of a subscriber 2 years. A GM (in theory) sub after the 6,000,000 install would bring $132 to GM in revenue share and $180 to XM.

>>>Keep on cheerleading–you certainly have the credentials to do so.

Huh? You talking to me? WTF? Where in my post was I “cheerleading”? Hey, whatever dude… I thought I was just helping you out with some more facts for your case. I only disagreed with one portion of your comment, regarding the recent sub increase — as I know for a fact that some of the other OEM installs are starting to hit the Gross side of sub additions now. How is that cheerleading???

Why don’t you try challenging individual facts in my post, instead of name calling. Then I can show you were I got my facts…

—

>>>XM calls the average life of a subscriber 2 years.

Tyler, are you sure about this? Where you referring to GM subs only? Or XM subs overall? Here is a quote from XM’s 10-K:

“Revenue from subscribers, which is generally billed in advance, consists of (i) fixed charges for service, which are recognized as the service is provided and (ii) non-refundable activation fees that are recognized ratably over the expected 40-month life of the customer relationship.”

40-months implies an average sub life of 3 years and 4 months. A sub life of 2-years implies churn of over 4% per month.

Regardless, with the current ramp of GM subs, XM is losing quite a bit of money on them currently — and will be for the next year, I estimate.

I put together a spreadsheet, starting with a base of 2.5 million GM subs, paying and ARPU of $10.32; using a churn rate of 1.7% per month; plus installation and activation of 2.5 million additional GM vehicles in 2008 (as well as 2009) straight line added over both years; at a SAC/CPGA expense of $100 per addition; with a 52% conversion rate to self-paying subs; and a payment to XM of $20 per promo sub; and finally a 50% revenue share with GM on all sub revenue from these subs.

Its a very rough model, but paints a decent picture for me of how much the ramp in GM subs is impacting the financials currently. For example, I estimate that these GM installs and revenue share cost XM approximately $16 million in Q1 this year — and will cost the company nearly $50 million for all of 2008. For 2009, I see it costing the company only $8 million — with the overall expense for GM subs finally going positive in Q4 next year… but that is assuming all the variables stay the same over the next 1.5 years (which is unlikely)… specifically: churn, ARPU, conversion rate and installation rate. Slight changes in those can impact the model easily.

Even more specifically to my spreadsheet, I estimated that XM started Q1 with 2.5 million self-paying GM subs and ended it with approximately 2.7 million; that XM Gross added 625K GM subs in the quarter, at a SAC/CPGA cost of $100 each ($62.5 million total); and after a 52% takeup from Q4 promo subs and a churn of 1.7% in each month against the base. These subs generated $92 million in self-pay (and promo paid) revenue, which was split 50/50 with GM.

The SAC/CPGA expense was $62.5 million added in with a revenue share of $46 million — ran the total to GM to $108 million… while XM was left with $46 million to cover the $62.5 million in SAC/CPGA expenses — thus the shortfall of $16 million in Q1. It can improve each quarter, provided the variables don’t change against them. If they can keep them in place, then these GM subs can pay off down the line.

The ramp is most certainly hurting this company right now. If XM is to be believed, then the deal isn’t quite as bad with Honda and the other newer OEM’s — which may offset some of this, but XM is certainly in a tough spot right now with this big jump in GM installs.

–

Homer….

You are correct. I was trying to point out that in two years, a GM sub will be close to being paid for. I was going to use the “lefe expectancy” aspect, but changed thoughts mid-stream. Thus, my statement was poorly worded. Where noonoe was saying that GM would get $400 to $500 compared to XM’s $50 is simply out of whack.

The “expected life” of a sub is 40 months for XM and 42 months for Sirius, but this is simply an accounting function more than anything else

In doing your analysis of the value of a sub you are leaving out the just under 200 per install that GM is paid for the two installs it takes to yeild one sub. Also you are not discounting the stream of revenue minus the total costs of the service (advertsisng,royalties, op costs, cap ex, etc) by the very high cost of funds. Similarly in figuring what GM makes you must add the bounty they are paid less the two month trial to the revenue stream. That brings GM to well over 400 per sub.

You guys also seem to confuse revenue with profit–SAC & TCPGA are just the marketing expenses of getting a sub–they do not include all the cost of providing a service both direct or prime costs and overhead. When you take that into account and the very high cost of funds that XM has and will have over the next few years as your discount rate it is nonsense that they recoup the install fees and to GM and other costs in 2 years. Out of wack is right on an assumption that they recoup these in 2 years on a GM sub.

I was referring this from a direct cost standpoint. Obviously no sub to date has been “profitable”.

You obviously are not an acct or a financial analyst and do not know how to do a lifetime value of a sub. First in the bcast business direct costs would include royalties, talent, deals like MLB, Oprah, etc., labor for engineers, billing etc. You then would pro ratta all of the fixed costs on some reasonable basis to get the figures for the life time value of the sub. As for GM the get about 160 bucks install fee per sub net after their costs of providing the am/fm sat vs just an am/fm. They also get an additional 100-200 per car from the dealers. They then get the revenue split over what is in excess of 4 years based on the churn they claim. In any case it seems to me that you really do not understand the way you do this financial analysis. Have you ever been a fin analyst?

By the way you revenue numbers per month are too high as they do not take into accg the discounting and what ARPU realy is. The 3 months free on every activation they did laast q, the increasing number of multi year plans and the family plans which can impact GM too. I find it odd how on the fly you do this stuff and the variance is always pro XM. I think that is why noone calls youa cheerleader. I mean if you are going to pronounce the Q better than most analysts think then you ought to tell us why and have the numbers. If XM won’t give them to you and you do not understand analysis then maybe you should not make financial pronouncements.

jw….

1. Noone is all over the place on his figures and is assigning way to many subscribers to GM.

2. By Direct cost we are referring to SAC and CPGA. Neither include programming, rev.share, etc. If you want to include those that is fine. The discuission was how fast it takes to recover money paid in subscriber aquisition costs (SAC). If you want to take it furter than that you can.

3. You are way off base on the GM deal. I would sugget you read the deal.

4. The discussion relative to what a sub brings in was a general discussion using the simple math of what GM is getting paid on vs. what is getting collected. GM is not paid on the NET (ARPU). GM is paid on what is collected. If we were discussing anything more than that, then ARPU might be appropriate.

5. Noone can call me a cheerleader if he wants. There are people who will disagree with him.

6. I did not pronounce the quarter better than most analysts. I did say that that they were “good” “okay” quarters. Kindly refer to this – https://siriusbuzz.com/satellite-radio-earnings-reports.php

7. I did say that XM’s quarter was not as bad as some of the “HEADLINES”. I did not really comment on the analysts side of the picture.

8. What numbers are you looking for? Did you not see the same numbers everyone else did?

noone….

>>>>>>In doing your analysis of the value of a sub you are leaving out the just under 200 per install that GM is paid for the two installs it takes to yeild one sub. Also you are not discounting the stream of revenue minus the total costs of the service (advertsisng,royalties, op costs, cap ex, etc) by the very high cost of funds. Similarly in figuring what GM makes you must add the bounty they are paid less the two month trial to the revenue stream. That brings GM to well over 400 per sub

Lets assume a $100 GM subsidy

Lets assume $20 in revenue from GM during the trial period.

Lets assume a $5.50 revenue share after a sub becomes self paying.

Lets assume a 53% take rate

Lets assume 1000 GM installs at a single point in time.

The subsidy is $100,000. The revenue back From GM is $20,000. So for we are at ($80,000) for XM. 470 subs drop Drop and 530 stay.

Those 530 pay $13 per month. GM gets $5.50 and XM gets $7.50 (per month). This translates to $2,915 per month to GM and $3,975 to XM. After 3.3 years, GM has received $116,600 in revenue share and XM has received $159,000.

XM is positive $79,000 and GM is positive $196,000.

If you want it is fine to devise a content and operations cost per sub, but that is not the excercise we were doing. The excercise was to see how long it took XM to recover costs associated with a GM sub.

>>> Thus, my statement was poorly worded.

I can’t believe you’re saying this. Your statement was WRONG. Obviously. As in sticking out like a sore thumb. Yet, you cannot admit you made a freaking mistake?

jw

While there is a lot in your posts to disagree with, there is one point that you are right on the money about — there is a tendency for commentators to not fully understand the concepts of costing and CVP analysis. Unfortunately, the professional analysts lack this experience, too, for the most part.

A lot of this has resulted from the vast interest amongst people who have no understanding of the accounting principles at work in these companies. As a result, we have had confusion on issues such as revenue vs. deferred revenue, direct vs. indirect costs, variable vs. fixed costs, and which costs are appropriate to consider for a particular purpose.

If one is trying to evaluate a contract, you want to evaluate incremental revenue and expense only (as adjusted by consideration for any step-cost functions, such as the cost of call centers). OTOH, if one is trying to estimate profit or loss from subscribers, the process is quite different. As a result of having so many commentators who do not understand these subjects, there is mass confusion.

Unfortunately, this confusion has extended to professional analysts. As a result, you get idiots like Citibank’s analyst projection 7 or 9 billion in synergies — obviously, not in the ball park.

If these companies can generate a billion in discounted synergies, it will be an accomplishment. Highly unlikely, unfortunately.

Hiippo…if you followed the discussion you would see that it was about the timeframe in which it takes to recover the costs….then subsequently noone shifted to an NPV of $50 for XM over the life of a sub. What I was trying to illustrate was that the $50 and $400 to $500 figure were off.

I am well aware of the average life of a sub. I have discussed it before. XM “recovers” activation fees at a faster rate than Sirius from the deferred revenue column, and I have pointed this out a long time ago.

I have also said in the past that if someone wanted to take all costs and divide it by the subs they could do so.

Even in ths discussion it should be noted that the revenue share is not a SAC or CPGA cost.

Noone is going all over the map.

For the “life of a sub” on the 1,000 installs GM gets $369 and XM $149. This includes subsidies for installs, GM’s two months of payments, revenue share, and a sub staying on board for 40 months after the promo. If one includes the promo, then GM’s $369 figure goes down to $342.