Satellite Radio Retail Trend Improves In March

The NPD data for March 2008 has been released, and the trend at retail is seeing improvement. For the first time in many months, one of the satellite radio companies saw less than a double digit decline in year over year comparisons. The NPD Group is the leading global provider of consumer and retail market research information for a wide range of industries. They provide critical consumer behavior and point-of-sale (POS) information and industry expertise across more industries than any other market research company.

March NPD retail is seeing both sector and individual improvement. The news is encouraging considering that the retail sector has been seen as a relative weak point in satellite radio. Getting to a consistent point that is measurable is a key to understanding where satellite radio as a concept is headed. The retail channel also offers insight into the minds of the consumer, as these radio sales are consumers who actually seek out the product rather than simply having it come as a feature in their car. Additionally, with no new receivers in the pipeline, this data starts to give an indication that is more free of existing subscribers simply “upgrading” their receivers.

The NPD data for March will likely be viewed in a positive light by the street as well as analysts, as the trend has improved substantially over the past three months. January’s NPD showed sector down 40%. February NPD had an improvement although sector sales were still down 17%. Now in March, sector sales are down 14% 11%. For Sirius the drop in year over year was only 8.7% 3%. This represents 31 consecutive months that NPD has shown Sirius to have a larger retail share than XM.

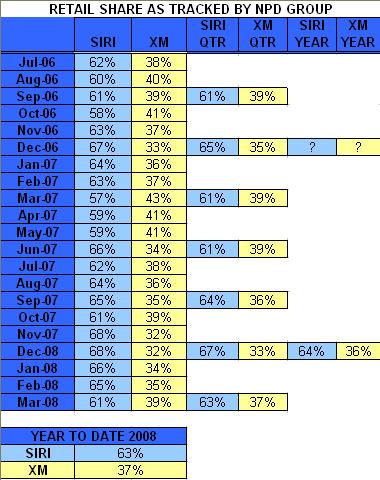

NPD MARKET SHARE MARCH 2008

Sirius – 61%

XMSR – 39%

YEAR TO DATE NPD MARKET SHARE 2008

Sirius – 63%

XMSR – 37%

Q1 2008 NPD MARKET SHARE

Sirius – 63%

XMSR – 37%

YEAR OVER YEAR COMPARISON (MARCH 2008 vs. MARCH 2007)

Sirius – Down 8.7% 3%

XMSR – Down 21.8%

Sector – Down 14% 11%

MONTH OVER MONTH COMPARISON (MARCH 2008 vs. FEBRUARY 2008)

Sirius – Down 3% Up 3%

XMSR – Up 23%

Sector – Up 6% Up 10%

Position – Long Sirius, Long XM

>>> This represents 31 consecutive quarters that NPD has shown Sirius to have a larger retail share than XM

31 quarters? Wouldn’t that be 7.75 years?

typo. now corrected. 31 months.

I have a theory for the reason SIRI is killing XMSR in retail. It is because people that get a GM, Toyota, Honda, are ripping their XMSR radios out to replace them with SIRI ones. The reason XMSR has gained in the last month is people can see now, that the DOJ approved of the merger, they think they will now be able to get the content on SIRI they originally wanted. Just a theory, LOL.

>>>I have a theory for the reason SIRI is killing XMSR in retail.

Since when does a 54% to 46% retail activation market share mean that Sirius is “killing XM”? Define “killing”. In my book, 54 to 46 does not equal a “killing”.

Retail activations are all that matters when trying to do the type of comparison that you are trying to make.

NPD has its place and purpose — using it to measure whether one is “killing” another in retail additions is NOT an accurate measurement.

This has been demonstrated over and over… and I’d be more than happy to demonstrate it again for you.

>>> I have a theory for the reason SIRI is killing XMSR in retail.

I was thinking Homer disproved your theory a month or two ago. Now you’re back with it?

THIS IS NOT COMPLICATED: NPD SHARE DOES NOT EQUATE TO RETAIL MARKET SHARE. EVEN TYLER HAS MADE THIS FACT CLEAR. Why are you not getting it?

Sorry, Homer, didn’t mean to shout over you — I didn’t see your reply until after I wrote mine.

But it is strange this fellow, after being corrected by you a month or two ago, is acting like that conversation never happened.

Seems some people will do everything they can to keep from seeing the truth — in this case, the truth being that the retail split is pretty close to 50/50, with the slight edge going to Sirius.

If one were to assume that NPD captures 40% of XM’s retail sales, then NPD would have to be capturing 68% of Sirius’ sales for retail to be an even 50/50 split.

I think that NPD capturing 68% of Sirius’ retail sales is a real stretch.

If you were to that NPD captures 40% of XM’s sales and Sirius’ sales at:

60% – then the retail split would be 53% SIRI and 47% XM

55% – then the retail split would be 55% SIRI and 45% XM

50% – then the retail split would be 57% SIRI and 43% XM

There are many factors involved. Sirius hardware tends to be at a higher price point at brick and mortar retail stores. This could impact consumer decision. The direct sales of the companies vary, the level of rebates vary, and the promotions vary. This could also impact the numbers.

Clearly at brick and mortar stores Sirius is outselling XM. Clearly XM has historically done more direct selling.

Tyler, I do not disupute your NPD numbers — or what you believe them to be. But what they are not is an accurate barometer of retail activations. There is a big difference between “retail sales” and “retail activations”…

Retail Sales are monitored by NPD, like you show. These are a cost to the company, via much of the SAC/CPGA related expenses.

Retail Activations are not monitored by NPD, and can only be estimated through statements made by both managements. While there is a slight cost to the company for these activations — these new “SUBS” also represent revenue coming in to the company.

Just because Sirius holds the edge (61/39) at “retail sales” — does not mean that Sirius is “killing XM” at retail. It just means that Sirius is selling more receivers than XM at monitored outlets.

However, with “Retail Activations”, the split is closer to 54/46 and this is IMHO where it matters more to me as a shareholder. Because this is where the revenue is coming in to the company… not just the expense.

Retail sales = a guarenteed expense to the company, with no guarantee of revenue.

Retail activation = a guaranteed expense AND guaranteed revenue to the company.

That is why I spend the time harping on one barometer over the other — and disputing claims of one “killing” the other. Because where it matters most to shareholders (revenue coming in), the split is no where near 61/39.

homer,

The distict diff between sales and activations does indeed exist and at this point should be well known to people.

NPD is a decent barometer when used properly.

Additionally, a retail sale does not translate into a subscriber. People upgrade units, and that does not mean a new subscriber was “born”. When this happens, it is still the same subscriber. This gets very problematic when a new device is launched and many people upgrade.

People will forever make comparisons. At brick and mortar stores, one is really dominating over the other. At non NPD channles, the domination swings to the other side.

There are many factors. A fully subsidized “free” radio will have more cost, but typically comes with a known term of service length.

Simply stated NPD needs to be used properly. NPD is a good barometer of what is happening at NPD covered stores, and NPD is a great barometer of what people are spending on average.

>>> Simply stated NPD needs to be used properly. NPD is a good barometer of what is happening at NPD covered stores

Everyone would agree with this, I think. But what is the ultimate value of a barometer of what is happening at only NPD covered stores, when that doesn’t reflect on retail activations?

Pretty much what I’m trying to say is that I disagree with blanket statements that claim Sirius “is killing XM” at retail. That is not substantiated in the general sense of what we define as the retail market. If people want to use the “killing” phrase, then they should quantify it as being an NPD sales figure — not “retail” as we know it to be.

Do you not see a value in knowing how many units are selling at the brick and mortar stores? Do you not think that a reasonable extrapolation can be arrived at using the data?

With NPD you get an indication of how a quarter is shaping up while the quarter is in process rather than 45 days after a quarter has ended.

By example, if retail sold 2,000,000 (exxageration done on purpose) radios in Q1, would you rather have an idea that this was happening during the quarter or to wait until the company announced it 45 days after the quarter ends?

If all analysts are saying retail is going to be off by 30%, wouldn’t you want an indication tha it was only 20%, or on the flip side off by 40%?

Retail sales do reflect on activations. Not every radio sold is activated, but many are. Knowing the trending is very important.

The ultimate barometer is utilizing as much data as possible, combined with reasonable assumptions.

First of all, as I said and was never disputed last month was; after taking all net retail adds that SIRI/XMSR were getting (as they showed from their own last quarter earnings call). That SIRI was at a 3 to 1 ratio before churn. I then put in churn of the 1 million (which is most likely less but I gave retail more credit then OEM) XMSR had over SIRI, and showed SIRI still had a 3 to 2 ratio even after churn. I then said that, sence I used all the net adds that each got, that at a 3 to 1 and 3 to 2 (with churn), that no matter what XMSR is doing it is not doing as well as what SIRI is doing. Also it shows when given a free choice SIRI has a clear 3 to 2 advantage. This is also being proven in Canada were SIRI is the over whelming favorite. All that was never disputed by homer895. This is easy to find out just go back and see for yourselves.

Homer, as I said it was a theory. Darwin had a theory. While I do think having a 3 to 2 ratio over your competitor is killing the competition, That would be arguementitive. But the rest of it (ripping out radios, and drop in share of retail for the month) was more or less a joke. The *LOL* was there to show that.

Homer985, my post was in the Feb. NPD article, dated Mar. 19th. My post was at Mar 21st at 6:27 AM. It was never disputed and was factual. Now some may say that it was disputed but that person has no memory, and refuse to scroll up or actually go back to see what was said.

John, you cannot compare NET subscribers (from any channel), when the size of the base are different sizes. I take that back, you can — but not for the purpose that you want it for.

You understand that even with equal churn rates, the company with a larger base will naturally have a higher churnout.

Assume two companies with equal churn adding near equal GROSS subscribers — however, one has a larger base than the other…

COMPANY A: 1,000 subscribers

COMPANY B: 1,500 subscribers

If the churn rate is 1.5%/month for both — then company A would churn out 15 subscribers, while company B would churn out 22 subscribers a month.

Just by the nature of Company B having a larger base — they naturally will have a higher churnout which would, in turn, skew the comparison that you are making.

The only way to trully compare whether one is “killing” the other (like you did), is by GROSS retail additions. Especially in light of the fact that Retail churn for each company is nearly identical and has remained consistent. It is no secret that XM’s retail base is larger than Sirius’.

Homer985, if you look at my numbers from my post at Mar. 21st 6:27 AM, you will see I used XMSRs churn rate and also figuered in the extra subscriber base for XMSR. That is why it gos from 3 to 1 ratio to a 3 to 2 radio after the extra churn is figured. As a matter of fact that was my main point, that even when extra churn is figured in it does not come close to making up the difference.

The fact is, over the whole retail channel SIRI has a 3 to 2 ratio over XMSR even when extra churn is figured in.

Now I do not understand you. You give your example that this was not already figured in, when if you look at my prior post, it absolutely is. Please go back and look at it. You can confirm my numbers with what XMSR/SIRI gave in there last earnings statement. I used their numbers, in net subcribers and churn rates.

>>>Now I do not understand you. You give your example that this was not already figured in, when if you look at my prior post, it absolutely is.

You cannot compare NET figures — because all things are not equal. The fact that you figured in “extra subscribers” to XM’s churn is a perfect example of why that comparison is flawed.

The fact remains — you flat out claimed that Sirius is “killing XM” at retail, when that is not at all accurate. Retail activations for all of 2007 were split 54% to 46%. That is not a “killing”. The fact that you are now trying to quantify this statement by saying you meant “NET figures” — and that you factored in “extra subscribers” for XM’s larger base, only goes against you. You’ve now entered in too many variable elements. Comparisons of RETAIL additions can only be compared using GROSS figures… not NET.

In fact, you said “SIRI was at a 3 to 1 ratio before churn” — however, that is not correct. That “3 to 1” ratio you’re starting with — appears to be the NPD figure… NOT the actual GROSS figure. And then you’re complicating it by throwing in your own estimation of churn to it, bringing it to a 3 to 2 ratio? I’m sorry, but that doesn’t make much sense. The starting ratio of ACTUAL retail activations was 5.4 to 4.6… not 3 to 1. If you’re not even starting off with the correct figures, then your end number will be no where near correct.

First I have always said it then and now, that is was net I was working with. If you had taken the time to go back and look at my prior post you would have seen that. I use Net because that is what counts, as a matter of fact that is the only number analyst care about when it comes to amounts of subs added. The only time you hear about gross subs is as a side note or if the nets are so bad they are used as a distraction. World Space is a perfect example of that. The net is most important, because you not only have to get people but it is more important to keep them.

It reminds me of a saying, it gos like this; there is a man on a boat that is taking on water at a rate of 10 gallons a minute but the man keeps saying thats fine because I am bailing out 9 and a half gallons a minute.

Here are the facts as reported by both SIRI/XMSR, and are mathematically true.

1) SIRI total net retail adds for 2007 were 598,883

2) XMSR total net retail adds for 2007 were 185,000

3) That mathematically works out to a ratio of just over 3 to 1.

4) XMSR stated monthly churn for the year was 1.75%

5) XMSR had a average of under 1 million retail subs more then SIRI for 2007.

6) 1.75% X 1 million = 17,500

7) 17,500 X 12 months = 210,000

8) 185,000 + 210,000 = 395,000

9) 598,883 to 395,000 works out to be just over a ratio of 3 to 2 after churn.

Those numbers are undisputable, unless you dont believe both SIRI/XMSR on their 2007 reports.

Homer seems to be trouncing you on the issue at hand, but I do have a couple of questions:

>>> I use Net because that is what counts

a) Then why do you care about NPD figures?

b) If “net” is what counts, does this mean the fact that Sirius spends some multiple of what XM does to get retail subs is without consequence?